- Feb 3, 2026

SoFi Stock Analysis 2026: The Path to $75 and S&P 500 Inclusion

The "Patient Investor" on YouTube has brought up a very interesting stock idea, which I’m going to analyze today. First we dive into his fundamentals. Then we map the Chart to find the best potential price to start buying into this digital banking disruptor.

Let’s get started.

The Fundamentals from Patient Investor

SoFi is a digital-first personal finance company and bank that is currently undergoing a significant shift in its business model to drive long-term profitability.

Here is a short summary of what the company is doing:

Shifting to a "Fee-Based" Model: SoFi is moving away from just being a traditional bank that holds loans on its own balance sheet. It is increasingly acting as a "middleman" (similar to Robinhood's business model), where it refers borrowers to third-party lenders and collects origination fees. This reduces SoFi's credit risk and improves its profit margins [02:07].

Rapid Member Expansion: The company has scaled aggressively, growing from 650,000 members to over 13.5 million. Despite this growth, they currently hold less than 10% of the U.S. adult population market share, leaving a large runway for further expansion [01:08].

Focus on Profitability: SoFi is in its second year of profitability, recently reporting 38% revenue growth and record adjusted EBITDA margins of 29% [00:42].

B2B Platform Services: In addition to consumer banking, SoFi operates a business-to-business platform that other financial companies (like Chime) have used to power their own services [01:40].

Acquisition Strategy: The company maintains a strong cash position and is actively looking for new acquisition opportunities to expand its ecosystem [04:02].

Financial Performance and Growth

Strong Earnings: SoFi's recent earnings report are "amazing," noting 38% revenue growth and record adjusted EBITDA margins of 29% [00:42].

Profitability: The company is now in its second year of profitability, with a net income margin of approximately 13% [00:51].

Member Growth: SoFi has grown from 650,000 members to over 13.5 million, yet it still holds less than 10% of the U.S. adult population market share, suggesting a massive runway for future growth [01:08].

Business Model Shift

Diversification: SoFi is shifting toward a "fee-based" revenue model, similar to Robinhood. Instead of holding all loans (and the associated credit risk) on their own balance sheet, they act as a middleman for certain loans, collecting origination fees while referring the risk to third-party lenders [02:07].

Reduced Risk: This strategy improves the company’s risk and margin profile because they aren't as exposed if a borrower defaults [03:02].

Valuation and Outlook

Attractive Valuation: The stock is currently trading at about 38 times earnings, which Patient Investor says is "really cheap" given that management guides for an earnings-per-share (EPS) compounded annual growth rate (CAGR) of 38% to 42% through 2028 [03:08].

Conservative Estimates: He notes that SoFi has a history of "sandbagging" (under-promising) and has beaten analyst estimates for eight consecutive quarters [05:36].

-

Price Targets:

Upcoming Catalyst: There is potential for SoFi to be included in the S&P 500 in 2026, which could serve as a significant short-term catalyst for the stock price [06:35].

In my opinion, SoFi has very solid fundamentals, and there’s huge growth potential because of the massive markets they operate in.

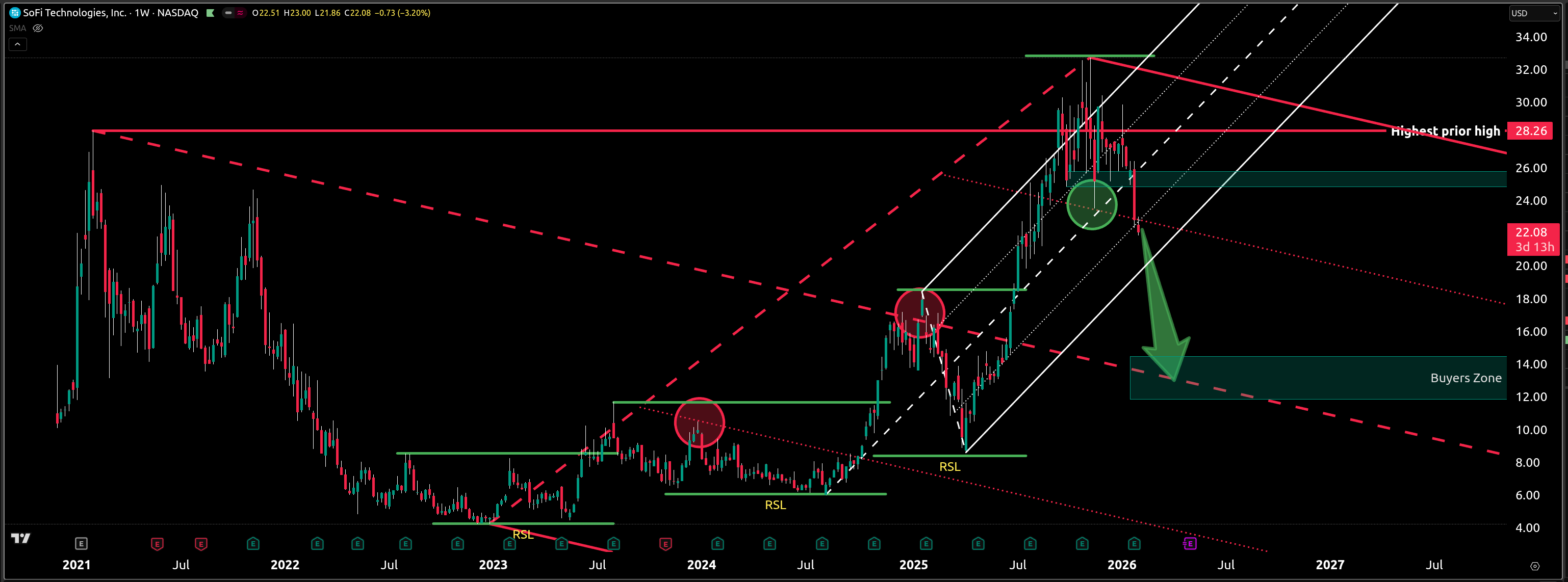

Now let's check the Charts to find the sweat-spot to buy into SoFi.

Chart Analysis

There you have it.

Our SoFi stock analysis is not only fundamentally strong. But we also see clearly where a potential real Dip-Buying level is to buy into this fintech growth stock.

If you liked this stock analysis, then subscribe to my newsletter. You will gain even more insights, learn about RealSwings and the Alan Andrews Pitchfork.

Talk soon

Emilio